Owning a home means investing in your future, despite mortgage rates. The housing market offers more than just a place to live; it provides financial growth.

High mortgage rates don’t deter housing market buyers

The truth about housing market and mortgage rates

Understanding the Long-Term Value of Real Estate Investments

In the long run, housing market trends show a consistent rise in property prices. This growth is not just a temporary spike but a sustained upward movement, making real estate a valuable long-term investment. It’s important to consider this when facing mortgage rates, as the eventual appreciation in property value can significantly offset these costs.

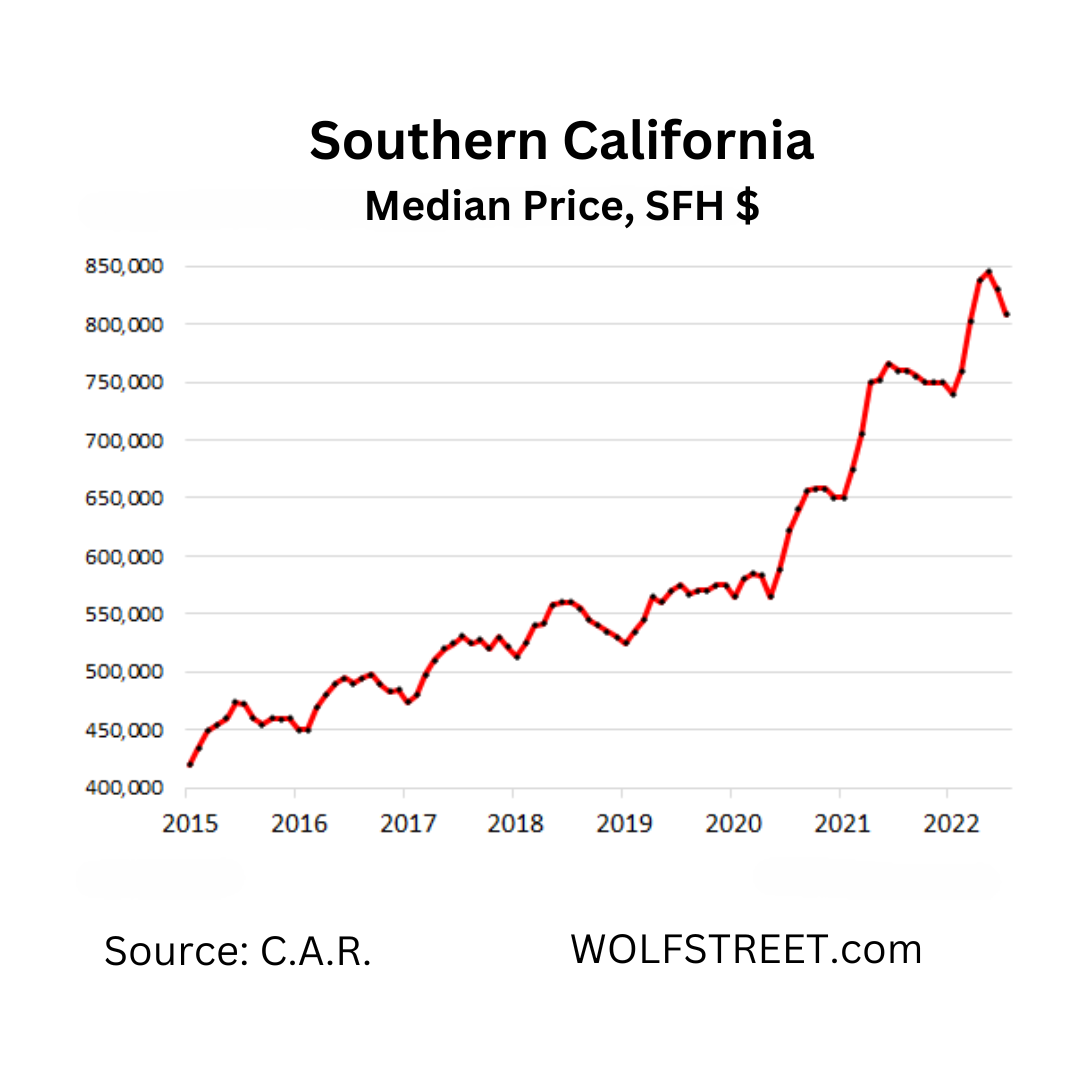

The Southern California Example

According to C.A.R., the real estate market in Southern California provides a clear example of this trend. In 2015, the average price of a single-family home was about $425,000. By 2022, these figures had risen dramatically, with house prices peaking at $850,000 – a 200% increase in value. This remarkable growth within the housing market is a testament to the long-term value of investing in real estate.

The Financial Benefits of Buying Over Renting

Let’s say you bought a $425,000 house in 2015, you need a $340,000 mortgage with a 4% interest rate. By 2022, you sell the house for $850,000. In general, this deal will bring you:

Sales value in 2022 (+) $ 850,000

Initial purchase (-) $ 425,000

Mortgage rates paid (-) $ 100,000

Gain (*) $ 325,000

(*) Excluding additional buying/selling costs.

In the scenario that you decided to rent from 2015 to 2022. The rent could have started at $1,500 per month. With an assumed annual rent increase of 3%, the monthly cost would rise to about $1,778 by 2022.

Over these seven years, you’d spend approximately $142,056 on rent. This full amount is your living expenses. It is completely dissolved. This is the opposite of the home buying scenario. Consider carefully: one side brings profit, the other side is just expenses.

The Importance of Location and Long-Term Planning

Remember that choosing the right location and having a long-term plan are crucial in the housing market. Paying mortgage rates in a promising area can lead to substantial gains. A strategic approach, focusing on long-term ownership, can make the mortgage rates you pay today translate into significant future value. It’s not just about buying a house; it’s about investing in the right part of the housing market and planning for the future.

Making Mortgage Rates Work for You

In conclusion, while mortgage rates are a necessary aspect of buying a home, the housing market’s potential for significant growth over time can make this a worthwhile investment. With the right location and a long-term strategy, paying mortgage rates can lead to substantial returns in the housing market.

Increasing house prices despite high mortgage rates

How Mortgage Rates result in gains and avoidance of rental waste?

How Buying a House Outweighs Renting in a Rising Market

Buying a house, even with mortgage rates, effectively addresses the problem of rent money feeling wasted. In a steadily rising housing market, renting can often seem like a financial drain, with each rent payment not contributing to any personal asset. In contrast, mortgage payments are an investment towards homeownership, turning a monthly expense into a long-term benefit.

The Cost of Renting: A Seven-Year Snapshot

Let’s revisit the rental scenario discussed earlier. Renting a house for seven consecutive years costs you about $142,000, an amount that escalates in a market where both property values and mortgage rates are on the rise.

After seven years, renters face the reality of having spent a significant amount of money, facing even higher future expenses, and drifting further away from the opportunity to purchase a home as property prices have surged by 200%.

When considering the cost of renting, it’s crucial not to focus solely on the monthly payments but to adopt a long-term perspective. Over time, not only do you lose a substantial sum of money, but you also forfeit the opportunity for homeownership, missing out on the chance to invest in your financial future and build equity.

Building Equity Through Homeownership

On the other hand, if your monthly mortgage payment is also $1,500, over the same period, not only have you paid a similar amount, but you’ve also made significant strides in building equity in your home.

For instance, if out of your $1,500 mortgage payment, $1,000 goes towards the loan principal and $500 towards the interest, after 10 years, you’ll have accumulated $120,000 in equity. This built equity is a tangible asset that you own, which is a stark contrast to rent payments that offer no return on investment.

Refinancing: A Strategy for High Mortgage Rates

Remember, in high mortgage rates situations, refinancing when market rates drop is a viable option, potentially reducing payments. The housing market often sees property values rise over time, balancing out the impact of initial mortgage rates.

The Long-Term Benefits of Buying a Home

In conclusion, despite mortgage rates, buying a home is financially sound. The housing market offers growth potential, turning mortgage rates into a worthwhile investment compared to the dead-end of renting.

Owning rather than renting even with mortgage rates

The most beneficial you’ve ever seen from Mortgage Rates!

Unlocking Tax Advantages in Homeownership

Purchasing a home, even with mortgage rates, offers a significant tax advantage, making it an attractive option in the housing market. The ability to deduct mortgage interest is a key financial benefit. While mortgage rates can initially seem challenging, the tax deductions available for mortgage interest can considerably lower yearly tax burdens.

The Financial Benefits of Mortgage Interest Deductions

In the early years of a mortgage, the majority of the payment often covers interest, leading to larger tax deductions. Even in a housing market where mortgage rates are high, these deductions are highly valuable.

Comparing Homeownership and Renting in the Tax Perspective

Assuming that you own a home and pay $15,000 yearly in mortgage interest with a 30% tax rate, you’re eligible for a $4,500 tax deduction. This deduction reduces your taxable income, offering a significant financial advantage to homeowners. In contrast, renters paying $1,500 monthly, or $18,000 annually, don’t receive such tax benefits. Rent expenses offer no tax deductions, leading to no tax savings.

This scenario highlights the financial perks of homeownership over renting, particularly the tax advantages of mortgage interest deductions. It’s a vital consideration for those debating between buying and renting, as these tax savings can substantially impact your financial situation.

The Long-Term Financial Impact of Homeownership

Historically, the housing market has demonstrated consistent growth, even in periods with fluctuating mortgage rates. This growth, coupled with the tax advantages of homeownership, further boosts the appeal of buying a home.

Making the Smart Financial Choice

In conclusion, the potential tax deductions available when dealing with mortgage rates make buying a home a financially wise decision in the housing market. It’s an investment that offers immediate tax benefits along with long-term growth.

Slash Taxes with homeownership, despite mortgage rates

Can you overcome the nightmare of Mortgage Rates?

Strategic decisions based on Mortgage Rates Insights

In summary, facing mortgage rates in the housing market can be daunting, but it’s a strategic financial decision. Historically, the housing market appreciates over time, and this long-term growth often surpasses the initial impact of mortgage rates.

Homeownership isn’t just about having a home; it’s an investment. Even with mortgage rates, the potential in the housing market is significant. It’s about building equity, not just paying off a loan. The tax benefits can often offset some of the mortgage rates.

The Wealth-Building Potential of Real Estate

Consider this: owning a home in a rising housing market builds wealth. Mortgage rates are temporary, but homeownership is lasting. The growth potential of the housing market turns mortgage rates into a smart investment.

In essence, buying a home, despite mortgage rates, is a savvy financial move. It’s a step towards financial security in a growing housing market. Don’t let mortgage rates deter you. The long-term gain of the housing market outweighs them, and the option to refinance can further enhance this benefit.

Investing in Your Future with Homeownership

Owning a home means investing in your future, despite mortgage rates. The housing market offers more than just a place to live; it provides financial growth. Today’s mortgage rates could lead to high rewards tomorrow.

So, take the leap. Mortgage rates shouldn’t stop your housing market dreams. Your future self will thank you. The housing market waits for no one, neither do mortgage rates.

Contact our team today http://danguard.com/services/ or at 800-560-5899 and take the first step towards securing your dream home and a prosperous future.

Conquer High Mortgage Rates: The Smart Path to Homeownership!

Also see: https://www.foxbusiness.com/real-estate